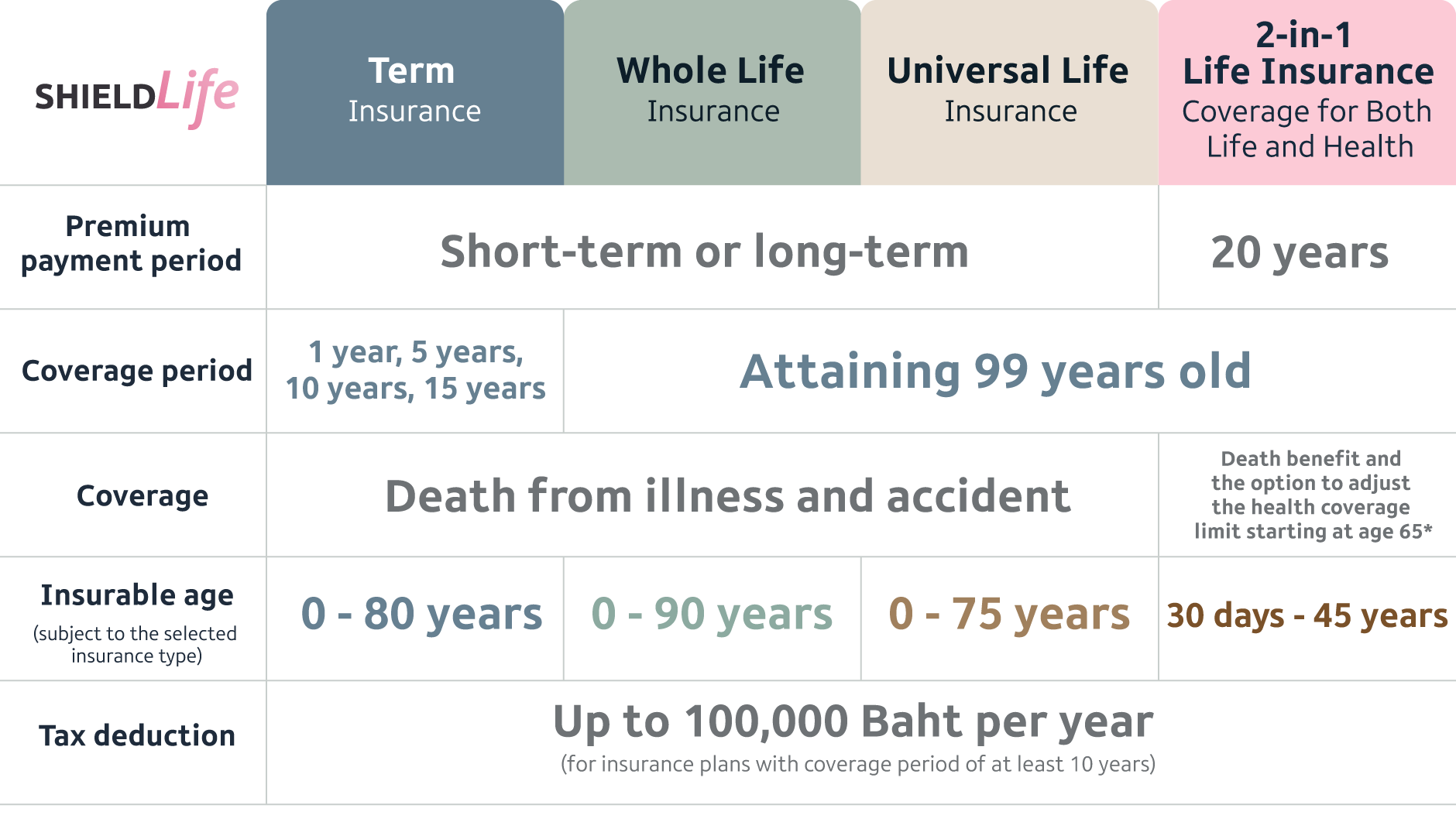

Q : What is the difference between term life insurance, whole life insurance, and universal life insurance?

A : The differences between each type of life insurance are as follows:

- Term Life Insurance: Provides coverage for a specified period, such as 1 year, 5 years, 10 years, or 15 years. Policyholders can choose the coverage period based on their needs. This type of insurance covers only death benefits. If the insured survives until the end of the policy term, no benefits are paid. Its advantage is affordable premiums with high coverage.

- Whole Life Insurance: Provides long-term coverage up to ages 90–99. It offers benefits in case of death as well as upon policy maturity. Some plans may also provide cash bonus during the policy term. It serves as a financial security throughout life,

with relatively moderate premiums—especially if purchased at a younger age.

- Universal Life Insurance: A life insurance plan combined with investment, clearly separating the protection component and the investment component. Policyholders have the opportunity to earn returns based on the Company’s investment performance, with a minimum guaranteed return. It is suitable for those seeking flexibility, as it allows adjustments to coverage and premium payments, as well as withdrawals from the policy value. This makes it adaptable to changing needs at different life stages and economic conditions.

Q: Can term life insurance premiums be used for tax deductions?

A : Yes, premiums for term life insurance can be used for tax deductions of up to 100,000 Baht per year, provided that the coverage period is at least 10 years.

Q : What is legacy life insurance?

A : Legacy life insurance is a policy that provides coverage in the event of death due to illness or accidents. It is designed to help pass on wealth to your family, enhance financial liquidity, and ease financial burdens such as home loans, car loans, business debts, or other liabilities.

Q : Is a medical check-up required to purchase life insurance?

A : Applicants are required to truthfully disclose their health information to the Company. A medical examination may be required depending on the policy criteria and the Company’s underwriting considerations.